Insight

In early 2026, gold reached record highs, supported by strong central bank demand and a global shift toward safe-haven assets. For investors looking to capitalise on this momentum, the traditional route of buying physical bullion is no longer the only option. Many investors are increasingly turning to Exchange-Traded Funds (ETFs), which offer a convenient and cost-efficient way to access the gold market through the stock exchange.

This blog explores how investors can navigate the gold market through Exchange-Traded Funds (ETFs). We will define the three core structures of gold ETFs, evaluate the strategic advantages of an ETF over physical bars, and provide an overview of the key considerations involved in gold ETF investing.

Whether positioned for long-term wealth preservation or tactical portfolio diversification, gold ETFs have become an increasingly important component of modern portfolio strategies.

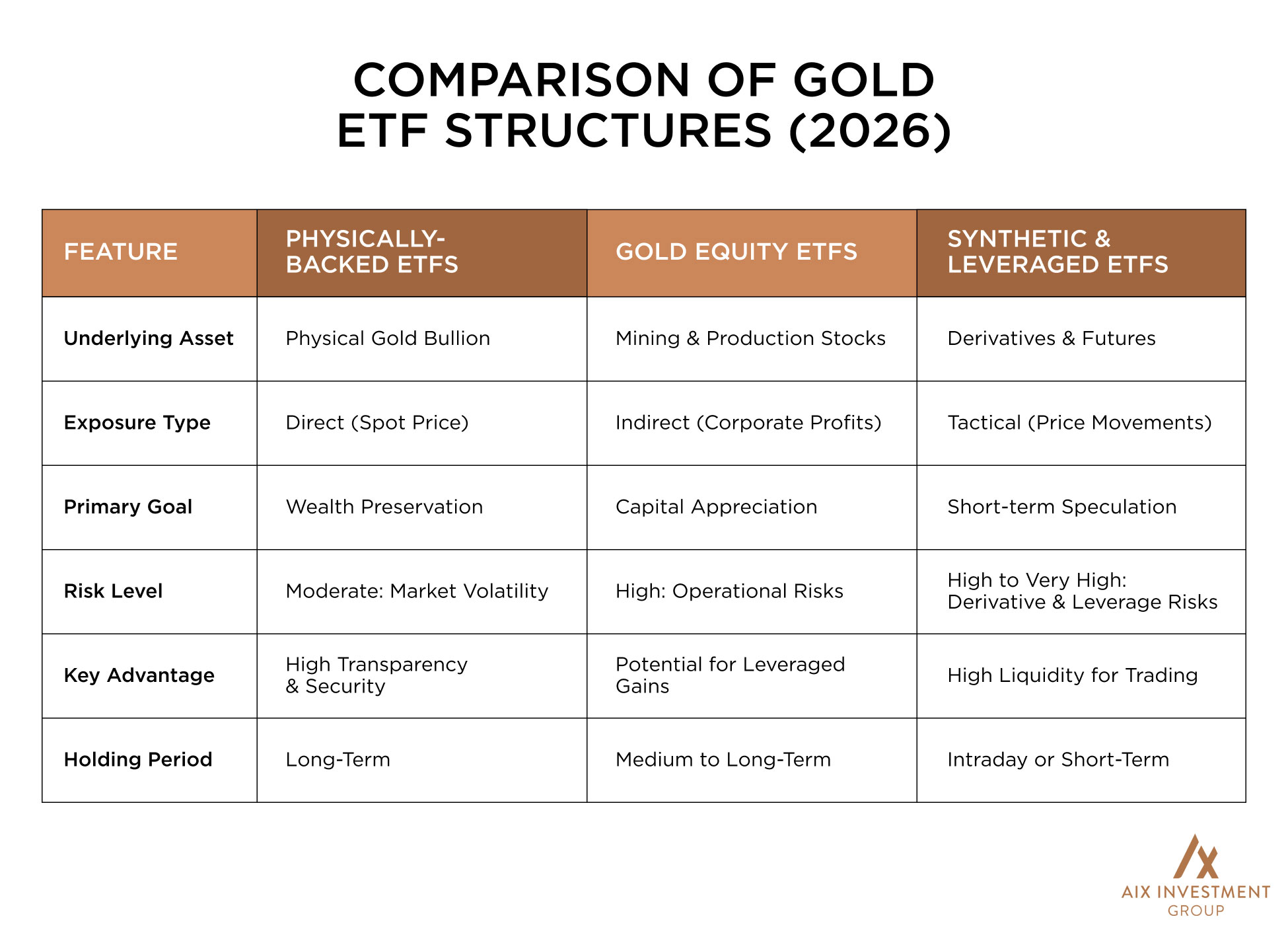

In technical terms, a gold ETF is a pooled investment security that operates much like a mutual fund but trades on a public stock exchange. Gold ETFs generally provide exposure to the gold market through one of three structures: physically-backed funds (direct metal exposure), equity-based funds (mining company exposure), or synthetic funds (futures-based exposure).

These funds purchase and store physical gold bullion in secure bank vaults. In this structure, each share represents a specific portion of that gold. When you buy a share, you gain exposure to a proportional interest in the fund’s gold holdings, allowing the share price to closely track the value of the underlying bullion. This structure provides direct exposure to the metal’s spot price and is commonly used by investors seeking long-term protection against inflation or currency devaluation.

These funds do not hold the physical metal itself; instead, they invest in a basket of stocks from companies involved in the mining, refining, and production of gold. Their performance is tied to the operational success and profitability of these companies as much as the spot price of the metal. Because mining companies may experience expanding profit margins during periods of rising gold prices, these ETFs can outperform the underlying gold price during favourable market conditions, while also introducing operational and corporate risks not typically associated with physical bullion.

Synthetic ETFs use derivatives and futures contracts to replicate gold price movements, while leveraged ETFs seek to magnify daily returns through the use of derivatives and borrowing. While these instruments are highly liquid and often used for short-term tactical positioning, they are generally more suited to active trading strategies than long-term wealth preservation. These instruments are subject to futures-market dynamics such as contango and backwardation. In prolonged periods of contango, the cost of rolling contracts can erode returns over time, while backwardation may have the opposite effect.

The growing preference for gold ETFs over physical bullion reflects several structural advantages within modern investment markets.

When starting an investment journey, you must understand the technical nuances that affect net returns:

In the United States, many physically backed gold ETFs are taxed similarly to direct investments in physical gold. As a result, long-term gains on certain gold ETF holdings may be subject to higher tax treatment than traditional equity investments, depending on jurisdiction and portfolio structure. Given the varying tax treatment across jurisdictions, professional tax guidance is often an important consideration when structuring precious metal exposure within a broader portfolio.

Beyond management fees, ETF pricing efficiency is also influenced by the bid-ask spread, which reflects the difference between market buying and selling prices. Higher-volume funds such as GLDM or IAU typically maintain narrower bid-ask spreads, helping investors minimize trading costs and improve execution efficiency.

Investors typically prioritise brokerage platforms with access to major international and regional exchanges, including markets such as the NYSE, LSE, or ADX. Platform selection is often influenced by features such as:

Fund evaluation often begins by comparing ETFs within the commodity or precious metals category. Key considerations include:

Portfolio exposure to gold is often calibrated according to broader diversification objectives, risk tolerance, and market conditions. During periods of substantial price appreciation, portfolio rebalancing may become necessary to maintain alignment with broader asset allocation objectives and risk parameters. This process may involve adjusting portfolio weightings to preserve diversification balance and maintain consistency with long-term investment strategy.

Gold ETFs continue to play an increasingly relevant role in modern portfolio construction, offering liquidity, accessibility, and diversified exposure to precious metals markets. By removing the traditional barriers of physical storage and insurance, these instruments support the integration of precious metals into diversified portfolios through a regulated exchange-traded structure. Whether investors prioritise the stability of physically-backed funds or the growth potential of mining equities, long-term outcomes are often shaped by disciplined portfolio management, allocation consistency, and ongoing market evaluation.

As investors evaluate the role of gold within diversified portfolios, investment decisions require careful consideration of market conditions, allocation strategy, and long-term risk management. In this environment, firms such as AIX provide strategic investment guidance across portfolio diversification, risk management, and long-term investment planning, including ETF evaluation and assessment of precious metals exposure within broader asset allocation frameworks. This supports investors in maintaining disciplined portfolios aligned with their long-term financial objectives.

For most individual investors, physical redemption is generally unavailable. In many gold ETFs, the creation and redemption of shares for physical bullion is restricted to institutional participants known as Authorised Participants, who transact in large creation units. Retail investors typically gain or exit exposure by buying or selling ETF shares on the exchange rather than redeeming them for physical gold.

Instead of sending you a bill, the fund manager gradually sells a tiny fraction of the gold held in the vault to cover storage and insurance. This is reflected in the “expense ratio” and slightly reduces the amount of gold each share represents over time.

A Gold ETF typically gains exposure through physical bullion holdings, futures contracts, or a combination of related assets. By contrast, a Gold ETN (Exchange-Traded Note) is an unsecured debt instrument issued by a financial institution that promises to deliver returns linked to a specified index or benchmark. If the issuing institution becomes insolvent, your investment is at risk, which is one reason ETFs are generally viewed as carrying lower counterparty risk.

Physically-backed ETFs do not, as gold produces no cash flow. However, Gold Equity ETFs (miners) often pay dividends derived from the mining companies’ operational profits.

Yes. Investors rely on the custodians (the bank holding the gold), trustees, fund managers and other service providers for safeguarding and administering the fund’s assets. While physically backed gold ETFs are typically subject to regulatory oversight, independent audits, and established custody arrangements, investors remain exposed to operational and custodial risks associated with these institutions.

Overview